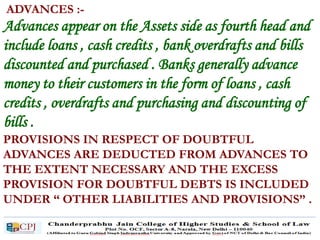

Summary

- Abc Quick

- Abc Typical

- Abc Higher

To invest in a property is among the most costly purchase you are likely and also make, so you may need assistance in funding it about function out of that loan. Let’s say you like it take a mortgage, however, after some time, end up incapable of afford the EMIs ? There is several reasons for which, off losing your job so you’re able to using up your coupons to own a medical exigency. Will the financial institution seize your house for individuals who miss 2-3 mortgage payments? Zero, maybe not quickly, but if you always standard to possess six months, the bank will need more your home.

Attaching a house ‘s the last thing a lender desires manage. Even if finance companies have the power to enforce the fresh new Securitisation and you will Repair off Monetary Possessions and you may Administration from Safety Appeal Work, 2002, (SARFAESI) to recover low-undertaking property without the intervention away from a court, this is basically the past step they like to take. A bank always allows you to definitely homeloan payment default sneak by the, but for another you to, it can send you a reminder to let you know that costs is actually later. Shortly after about three non-payments, the lending company will send a demand find, asking to expend the dues as soon as possible.

In the event the borrower will not respond to all e-mails, the financial institution directs an appropriate notice and their courtroom service, states VN Kulkarni, chief counselor from the Abhay Borrowing from the bank Therapy Center, which is backed by Bank of India. A bank waits for three months just before declaring an asset a beneficial non-performing one to. Pursuing the end of this months, the lending company can technically label the home loan a keen NPA and you may begin the process of healing the house or property from SARFAESI Operate, says Kulkarni. Even after invoking the latest Work, the financial institution offers the borrower a two-few days find period to repay the brand new fees.

Ultimately, five weeks following the earliest standard, the bank sends a notification, saying that it offers appreciated the property to possess a particular contribution and this have a tendency to public auction our house towards a certain big date. This is usually in for 1 month throughout the time one to the financial institution e-mails you the auction observe, contributes Kulkarni.

States Pankaaj Maalde, direct, financial believed, Apnapaisa: Finance companies and you can loan providers be much more trying to find healing the bucks than in starting courtroom proceedings because procedure for tying and auctioning property is lengthy and you can does take time. So, might pursue the challenge for at least half a year before getting legal action.

The very last stage can be whenever a borrower will get a notification from the Debt Healing Tribunal (to have mortgage levels of more Rs ten lakh).

Its required about how to sit-in the newest reading that is put by tribunal, where you could come to a contract for the lender. If you find yourself dedicated to using your own expenses and also have a an effective repayment track record, the lending company could well be prepared to give a flexibility.

The first step that the financial takes will be to understand the reason behind the newest default as the a mortgage is actually a protected one, for the bank having more control along side resource.

In the event that a lender is fulfilled your issue is genuine and the borrower may start make payment on EMI soon, it will be prepared to await some more big date. Although not, banking institutions bring particularly decisions into the an incident-to-situation base, says Maalde.

Contributes Rajiv Raj, movie director of CreditVidya: Extremely loan providers just take a functional look at the difficulty and you may understand exactly how crucial the house is actually for the person. So that they often directly connect to the new debtor knowing the cause for this new financial hardship.

Actually, a bank assists you to recover your home even after it’s captured it, regardless of if it has got as complete till the public auction occurs. States Kulkarni: Even when the auction go out might have been revealed, the brand new debtor may come into the any kind of time phase and you can spend the money for fees to save his possessions. Yet not, when your bank keeps incurred people charges for proclaiming the fresh new auction, this new borrower would need to spend such.

If you’ve missing your job, but they are pretty sure of getting a unique you to contained in this half a year, you can inquire the financial institution to offer you a moratorium for this period. But not, if for example the cash try burdened because of various other cause, such as the EMI increasing on account of a hike inside the rates of interest or increase in personal costs, inquire the lending company to help you reconstitute your loan. So you’re able to both slow down the EMI otherwise ensure that it it is at the same height despite increased interest, you could potentially improve the mortgage tenure.

When you have drawn an insurance rates tool, that also will bring a cover to possess death of business, the insurance coverage providers covers the newest EMIs for three weeks on time that you destroyed your job. For instance, ICICI Lombard’s Safe Mind Fitness package provides a cover for 9 significant scientific afflictions and procedures, dying and you can long lasting total impairment because of collision and you may death of job.

Within the plan, the new insurer pays three EMIs on the people financing which you have taken for many who cure your work. New hitch is that the job losses is going to be because of retrenchment, layoff or fitness explanations, and never since you were fired. Including, if you may take a wages equal to the the mortgage amount, the insurance policy period is only five years. The primary reason you ought to start paying the EMI once more, aside from to avoid hands of your house because of the lender, should be to ensure that your credit rating isnt adversely influenced.

Regarding 30% of your credit rating will be based upon fees record and a high element of this constantly relies on just how daily your pay off your house loan, when you have drawn you to definitely. Actually two skipped costs normally negatively feeling your credit get, and a continuing standard tend to damage it honestly, making it difficult to find financing otherwise credit cards on the future. As this is a serious circumstances, you can dip to your offers and you will old-age kitty and you will redeem your financial investments to expend the fresh EMIs. But not, whether or not it seems that the issue might not improve even with 6 months, a much better idea is to promote the home.

You could correspond with the lending company about it and make use of new sales continues so you’re able to prepay the mortgage. Yet not, make sure since business negotiations take, you keep up paying the EMIs. This will persuade the financial institution that you are not providing they getting a journey and can ensure that your credit score does not drop.

Read more development to the

- savings

- monetary believed

- investments

- EMI

- interest rates

- insurance